Ho Chi Minh City, Q1 2025

Economic Outlook

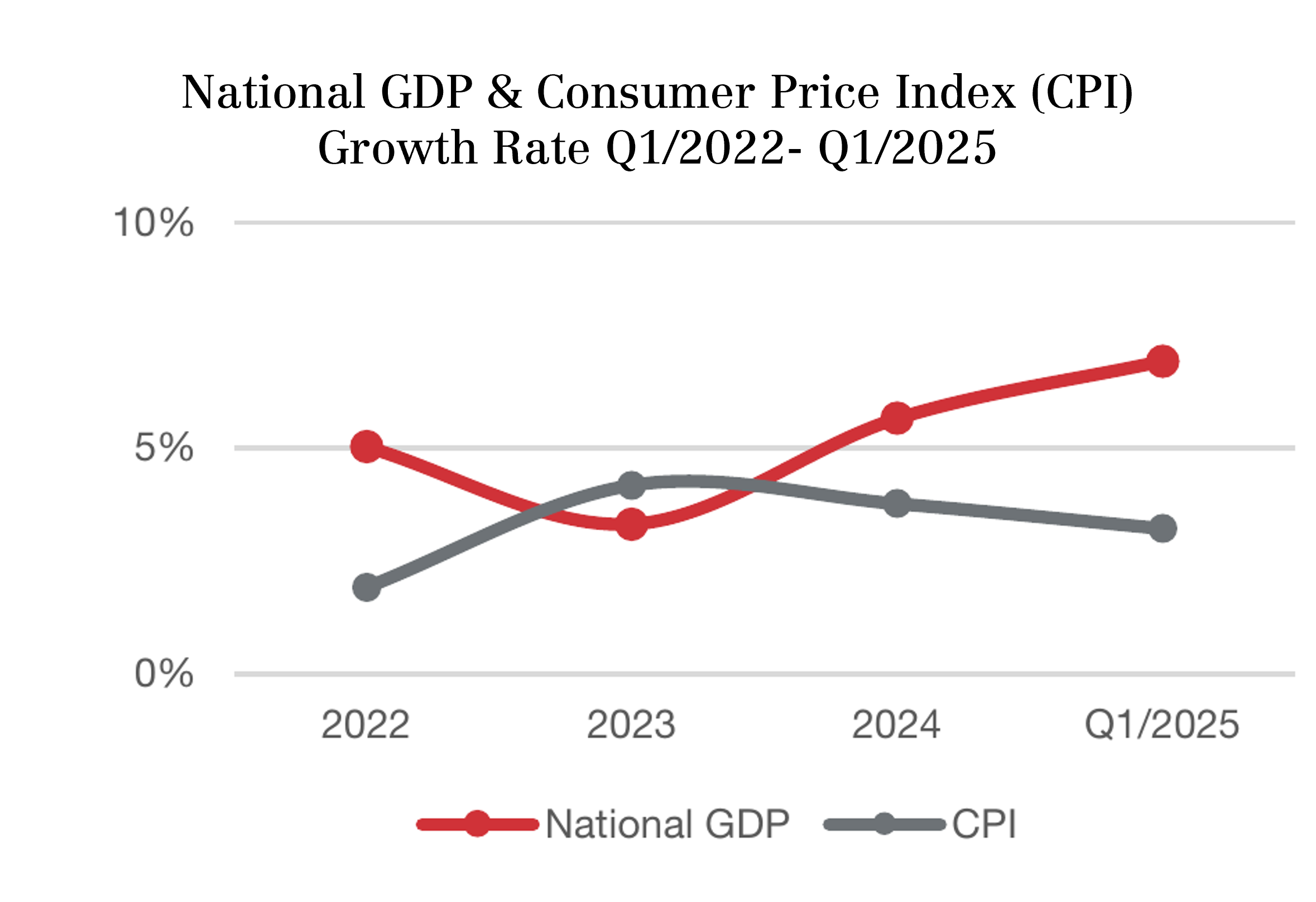

Amid global challenges, in Q1/2025, the GDP shows a growth of 6.9% year-on-year (YoY), marking the strongest Q1 growth since 2020. Vietnam also recorded over 72,900 businesses newly registered or resuming operations, marking a 54.8% YoY increase. Meanwhile, approximately 78,800 businesses exited the market during this period, a 7.0% increase from the previous year.

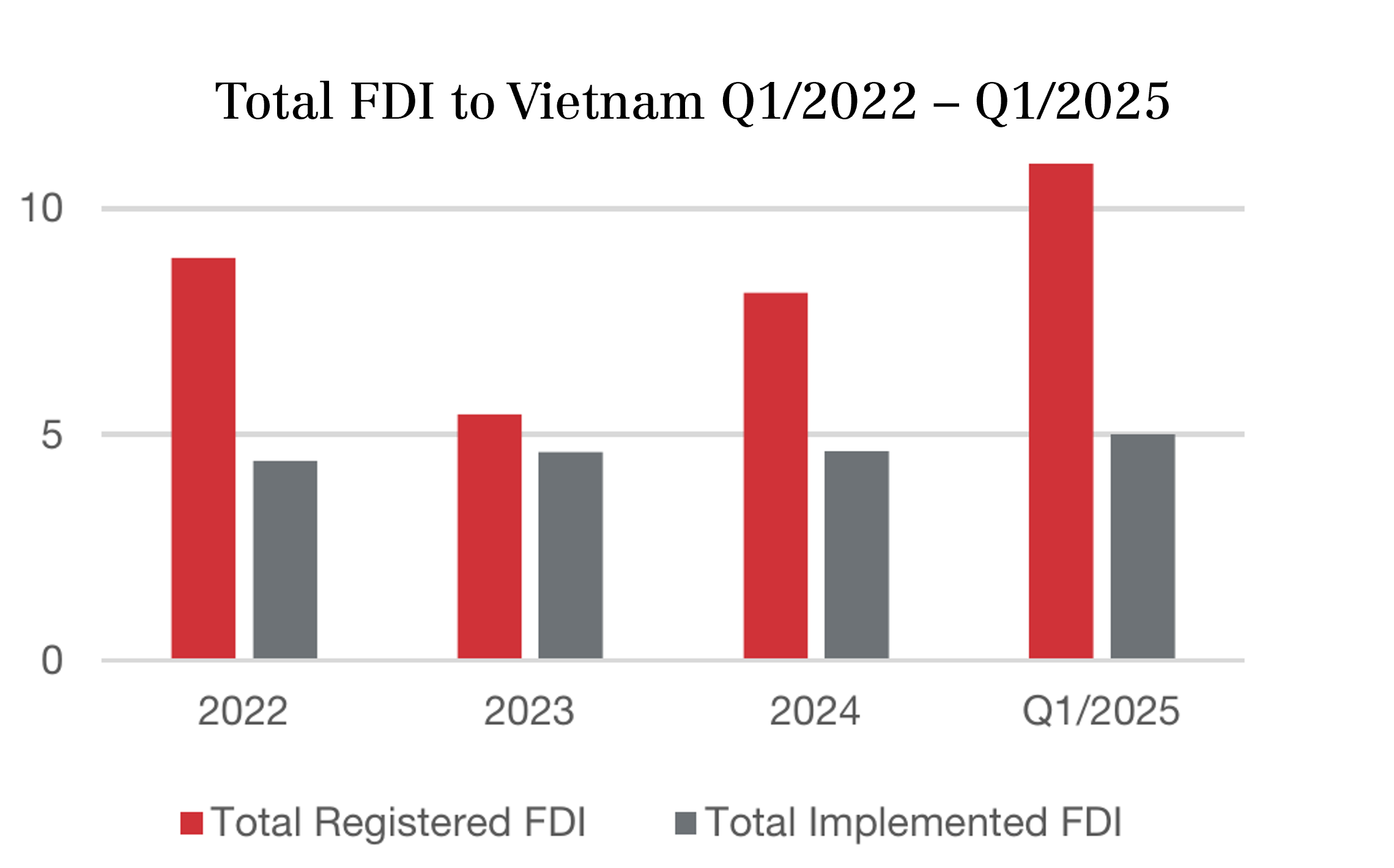

Foreign direct investment (FDI) registrations increased by 34.7% YoY to nearly US$11 billion. The amount of implemented FDI also reached nearly $5 billion, reflecting a 7.2% increase YoY.

The manufacturing and processing sector attracted $4.1 billion, accounting for 81.7% of the total implemented FDI. The top four investors in Q1/2025, in order, were Singapore (30.5%), China (28.5%), Taiwan (8.5%), and Japan (7.9%).

The total revenue from retail sales of consumer goods and services reached US$ 65.4 billion, up 14.9% compared to the same period last year, marking the highest growth rate for the same period since 2021.

HCMC Office Performance

Stable Supply

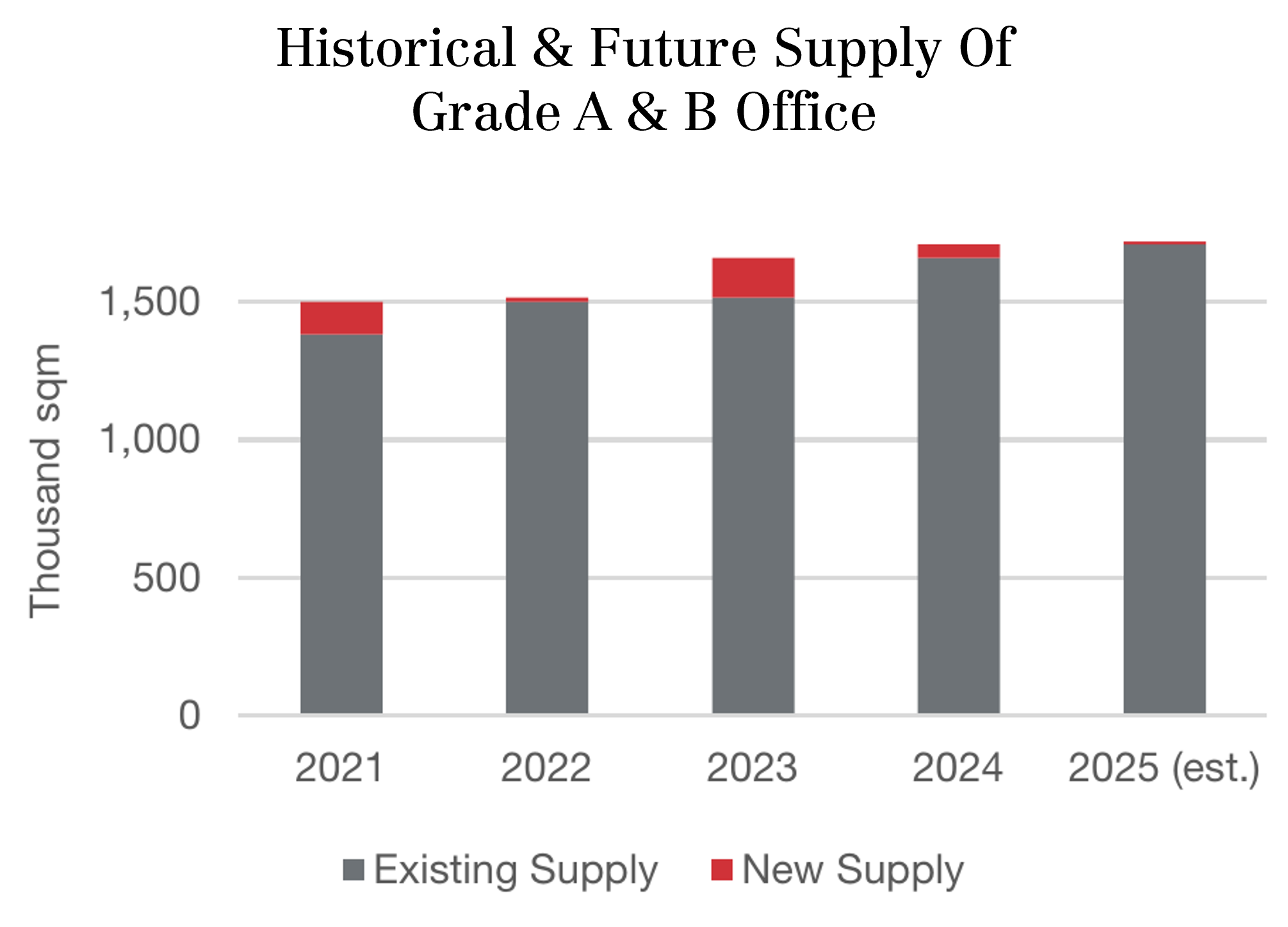

No additional Grade A or B office space was added to the Ho Chi Minh (HCM) market in Q1/2025, keeping the current supply stable at roughly 1.7 million square meters (sqm).

Stable Performance

The average net rental rate of Grade A remained stable QoQ, and increased by 1.5% YoY, at US$ 59.5/sqm/month in Q1/2025. Grade A buildings vacancies decreased in this quarter, with occupancy rate at 88.5%, up by 1.4 percentage points (ppt) QoQ and remained the same YoY.

Grade B net rent is stable QoQ at US$ 36.5/sqm/month but increased by 3.0% YoY. The occupancy rate reached 88.6%, down 0.8 ppt QoQ but improved by 1.1 ppt YoY.

Outlook

Key incoming new pipeline is Marina Central Tower, Grade A in Q2/2025. This quarter, older buildings with smaller leasable areas saw tenant departures. The competition in the office market is fierce as new buildings prioritize green, comfortable environments to satisfy the potential clients’ needs.

HCMC Retail Performance

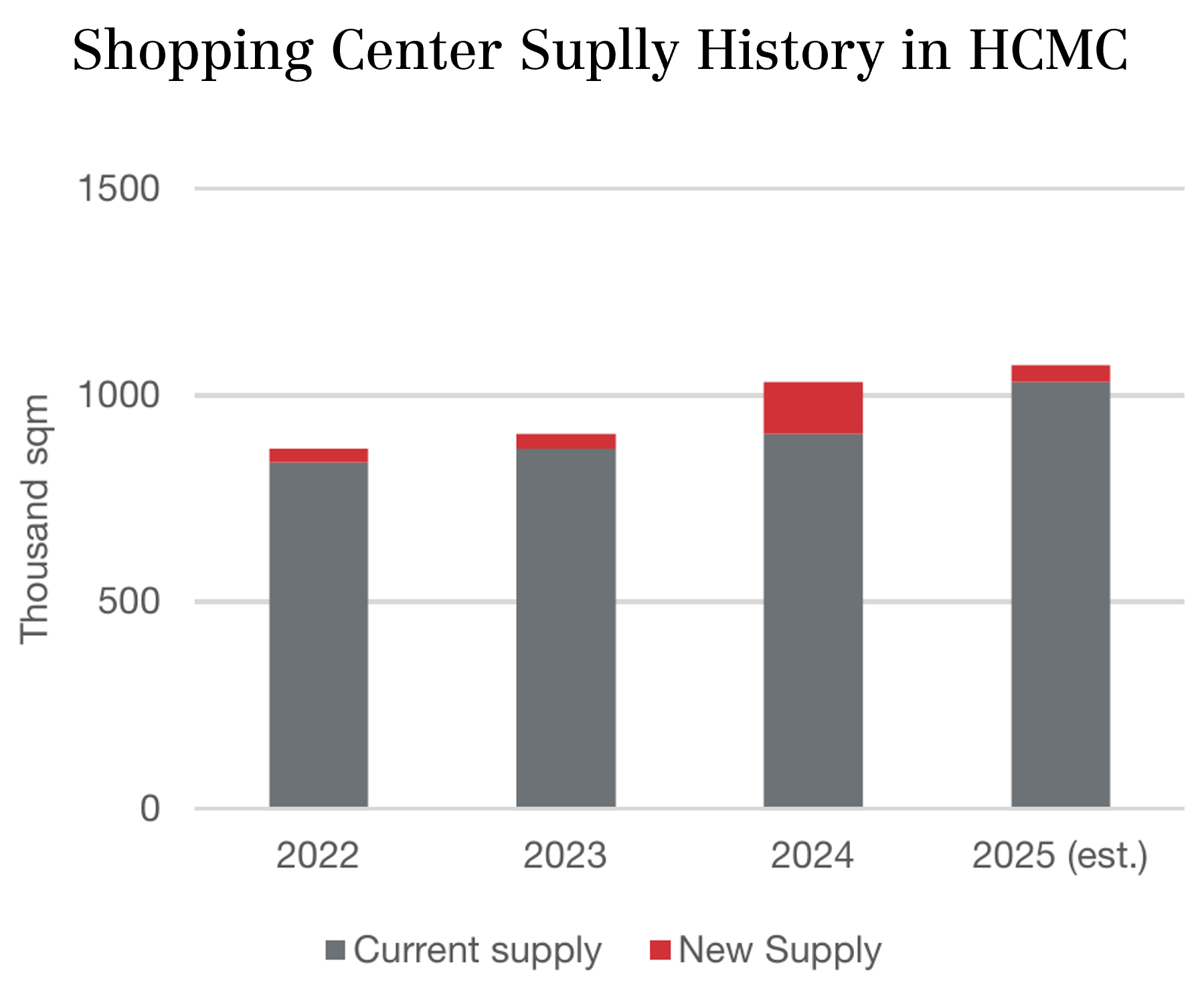

Additional Stock

In Q1/2025, the retail market saw an increase in supply as Centre Mall Vo Van Kiet in District 6 contributes an additional 15,000 sqm of shopping center space.

Stable Performance

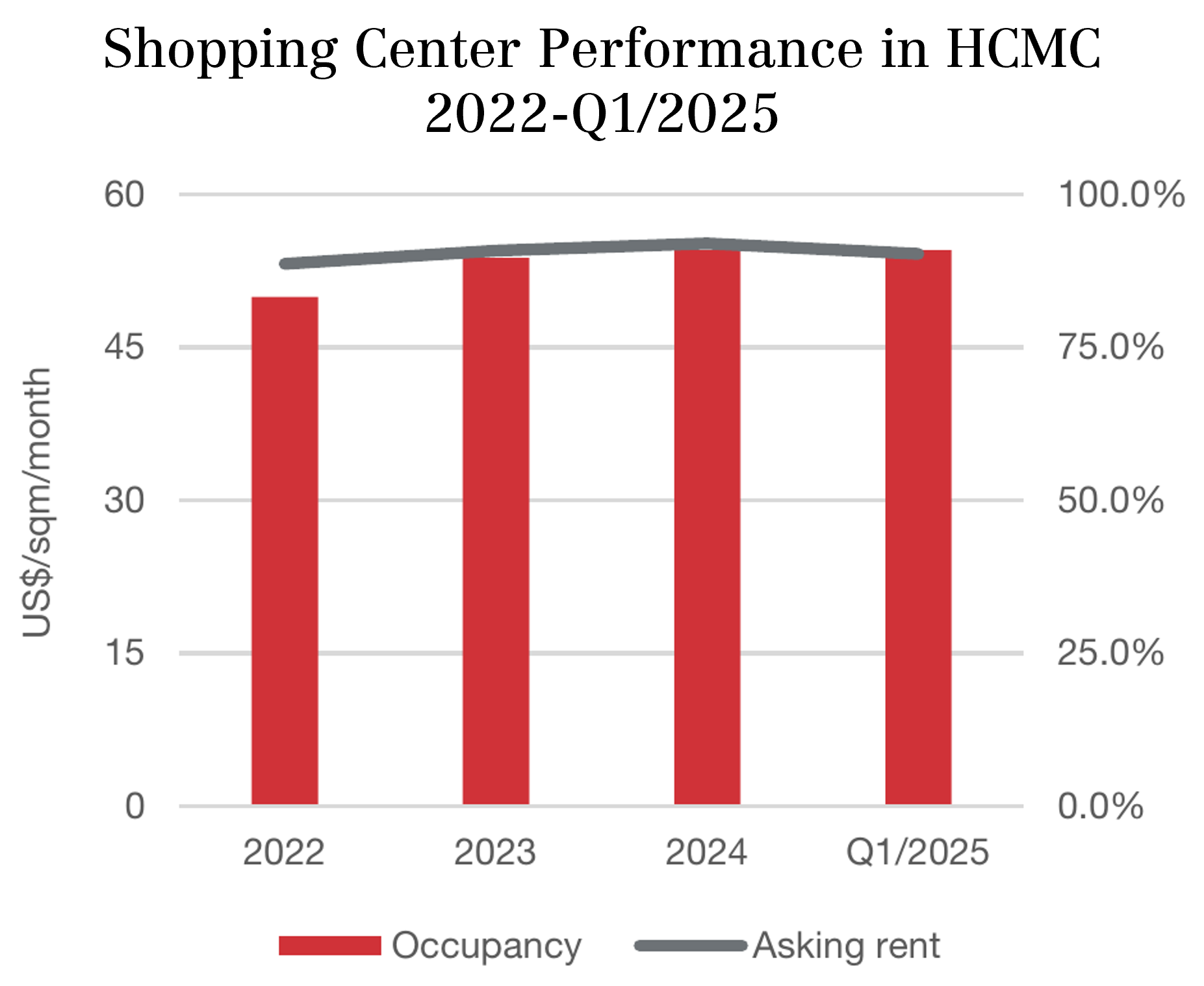

The average asking rent price for shopping centers in HCMC is US$ 54.2/sqm/month in Q1/2025, experienced a minor decline of 0.4% QoQ and a fall of 1.8% YoY. Despite recording new supply, the market-wide occupancy rate reached 91.0%, increased by 1.3 ppt QoQ and a small 0.1 ppt YoY thanks to the strong decrease of vacancy of Parc Mall and Central Premium Mall in District 8.

Outlook

In the upcoming quarter, more supply is expected to enter the market, especially in the CBD. The mass retail segment is expected to have positive performance due to greater tourism and strong growth in local consumption. It is forecasted that the retail market will continue to experience growth as Vietnam’s economy shows stronger growth potential after Q1/2025. Despite the increased supply, competition for shopping mall space is expected to remain fierce, as large spaces that can adequately meet consumers’ recreational and F&B needs remain extremely scarce.

South Vietnam Industrial Performance

Stable Supply

As of March 2025, several industrial parks (IPs) were approved for investment policies in Ba Ria – Vung Tau (2 IPs – 838 ha) and Binh Phuoc (1 IP – 483 ha). However, in Q1/2025, the IP supply remains stable.

Stable Performance

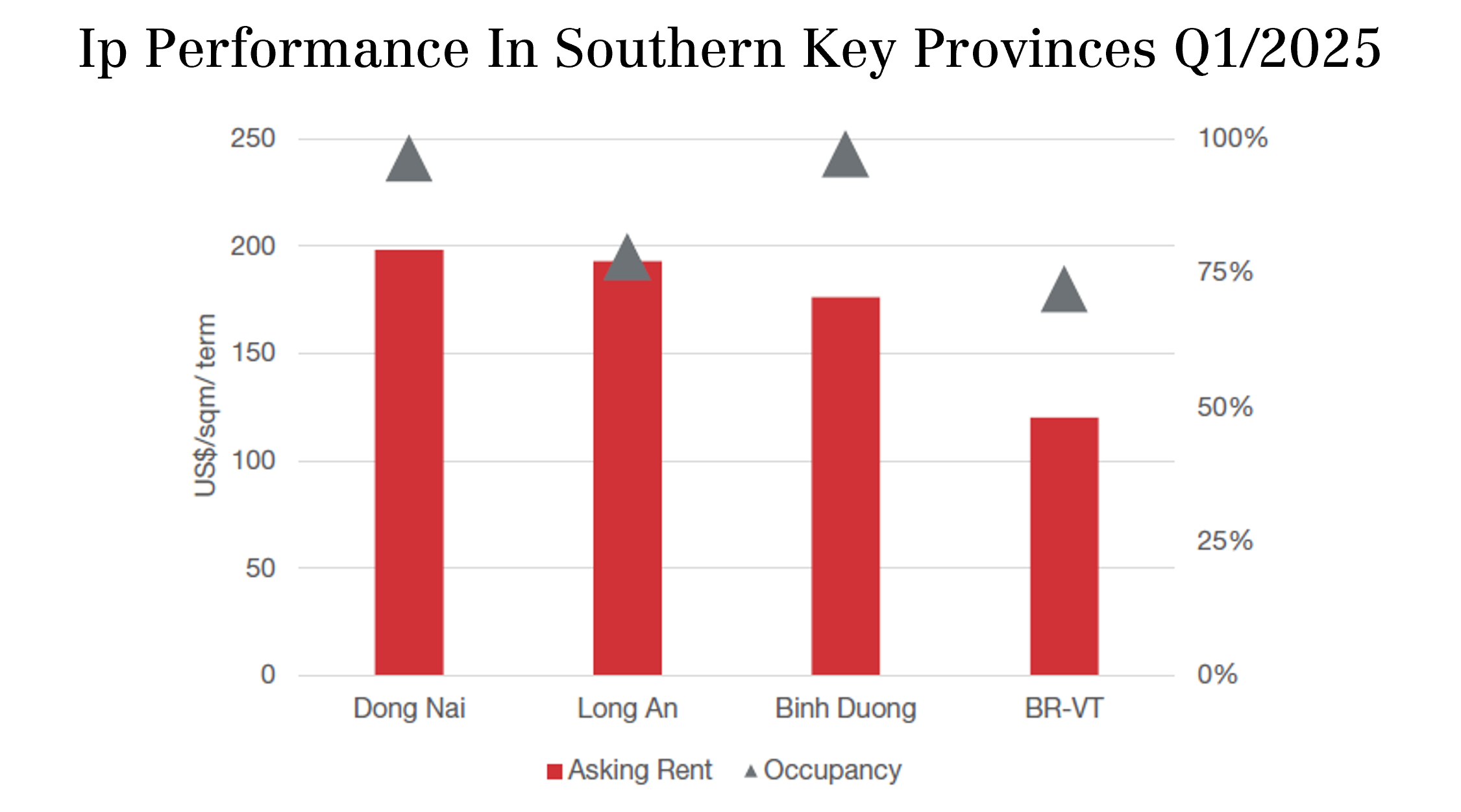

The average asking price for industrial land in key southern provinces rosed by 0.8% QoQ, reaching an average of US$ 175.2 per sqm/term. Meanwhile, the occupancy rate in the market is stable at roughly 90%.

Outlook

Uncertainty increases due to United States (US) government tariff policies affecting FDI flows, impacting industrial park real estate. However, higher tariffs on Chinese goods may accelerate manufacturing relocation from China to Vietnam.

From 2024-2027, Vietnam plans to add 15,200 hectares of industrial land, attracting new-generation FDI (high-tech, semiconductor, green energy) from US, China, and EU, promoting development of specialized high-standard industrial parks.

Disclaimer

This research has been prepared by NAI Vietnam for informational purposes only and should not be considered investment or legal advice.

This research report has been prepared independently and solely on the basis of publicly available information that NAI Vietnam considers to be reliable but NAI Vietnam has not independently verified the contents hereof. NAI Vietnam accepts no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts and reflect their opinion as of the date hereof. These opinions are subject to change and NAI Vietnam does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without NAI Vietnam’s prior written consent.