Economic Outlook

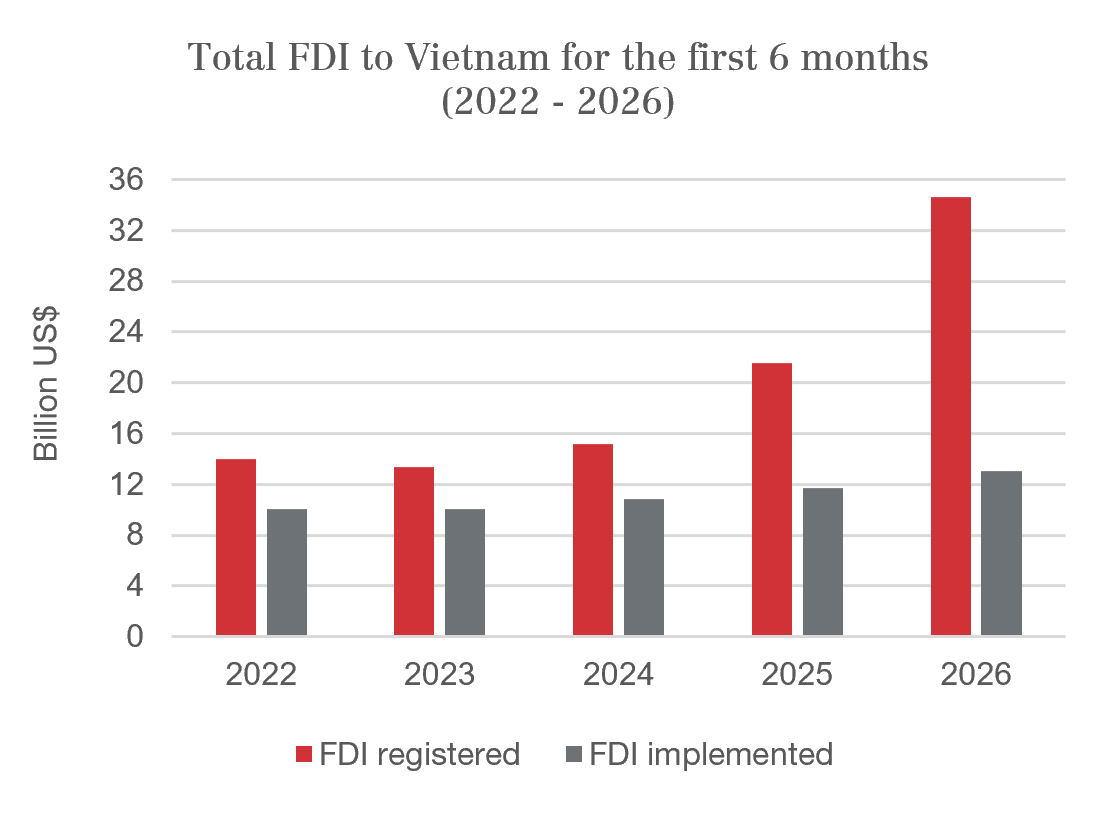

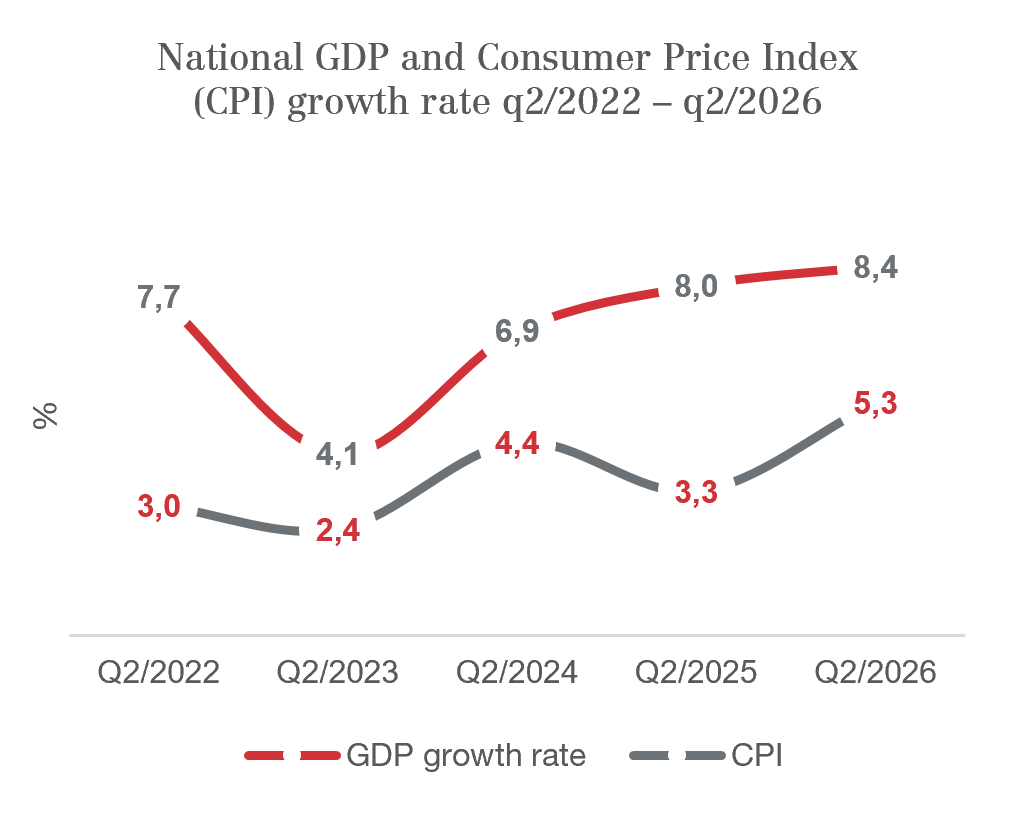

In Q2/2026, Vietnam’s GDP grew by 8.4% compared to the same quarter of last year. FDI inflows continued to improve in the first six months of 2026, with total registered capital reaching US$34.7 billion, a 61% increase compared to the same period last year.

Nevertheless, the trade deficit rose to US$16.7 billion in the first six months of 2026 due to rising raw material imports. This was likely driven by seasonal electronics and components demand for manufacturing preparation for Q3 and policy-driven demand for E10 bioethanol production, indicating economic expansion. However, a prolonged deficit will potentially pressure the exchange rate, ultimately driving up both import and manufacturing costs for firms.

The quarter also saw 96,000 new or resumed businesses, against roughly 91,800 market exits, pointing to intensifying competitive pressure. Heightened global geopolitical tensions, particularly in the Middle East and Gulf region, continue to pose external risks to trade flows, input costs, and overall economic stability in the quarters ahead.

HCMC Office Performance

Supply

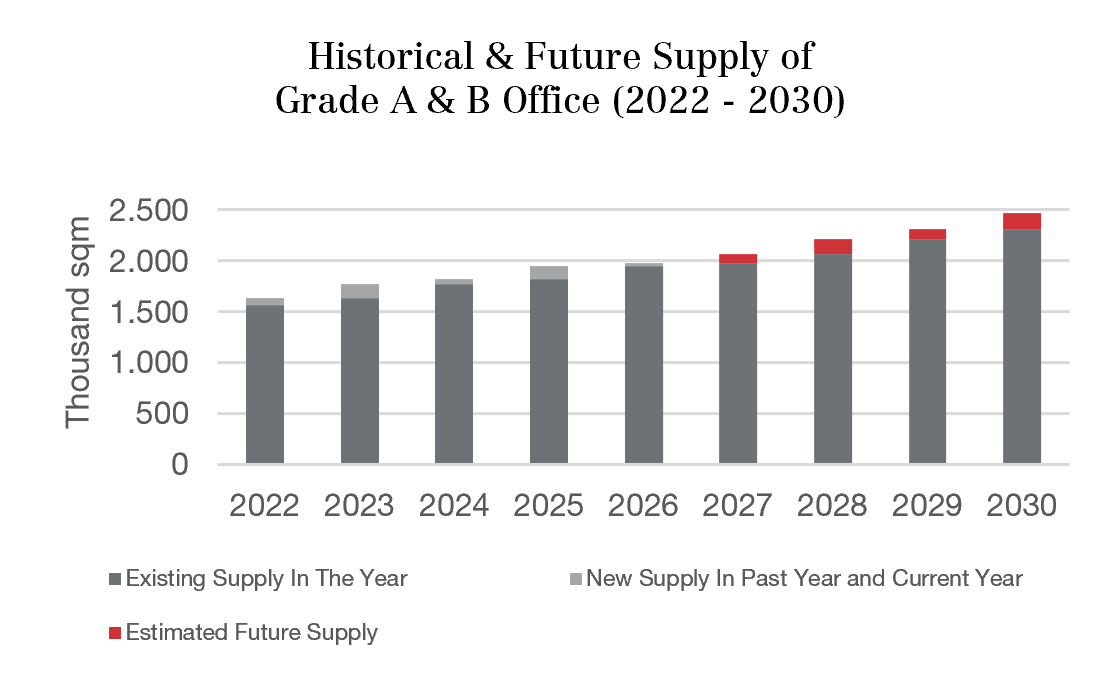

HCMC’s office market held stable at 1.8 million sqm in Q2/2026, but will approach 1.9 million sqm next quarter with the launch of The Kross (33,400 sqm), the year’s only new Grade A supply.

Performance

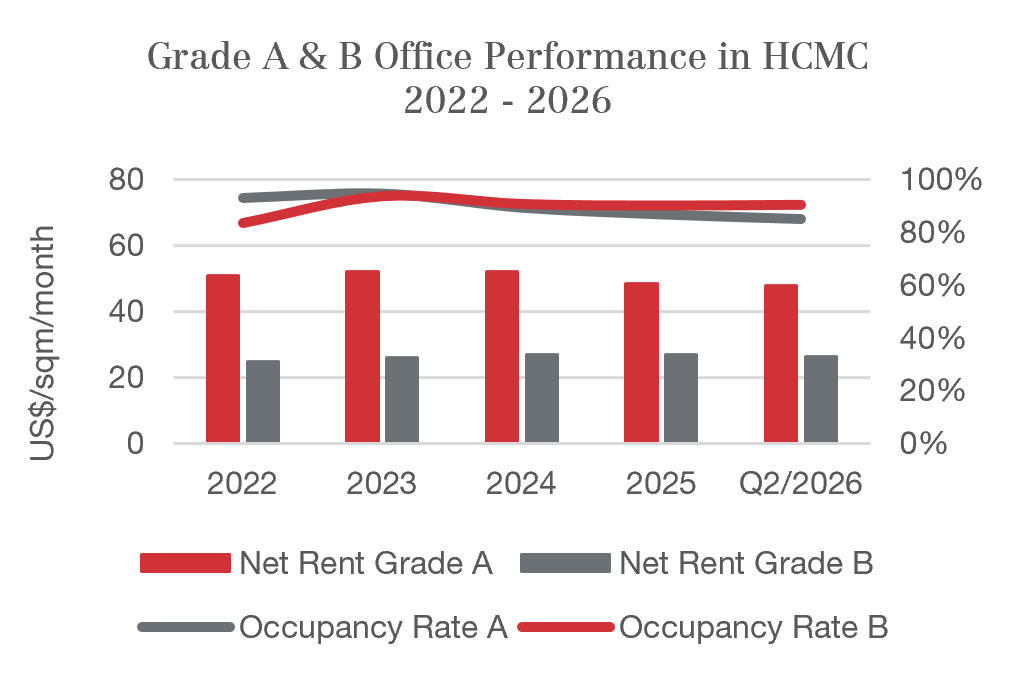

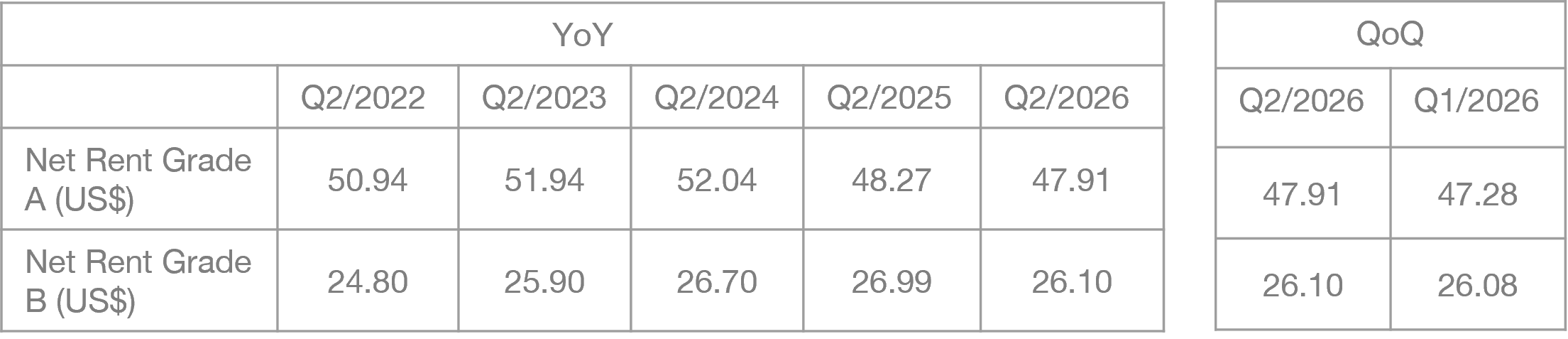

Q2/2026 was fueled by renewals and relocations in some notable sectors such as Finance and Information Technology. In Q2/2026, the overall Grade A office market averaged US$47.9/sqm/month, up 1.3% QoQ despite a 0.7% YoY decline. Occupancy improved 0.6 percentage points QoQ to 85.1%, though it remains down 2% YoY. While steady QoQ absorption highlights a recovering market, Grade A rents diverge significantly by location, averaging US$53.4/sqm/month in the CBD versus US$35.5/sqm/month in Non-CBD areas.

Grade B buildings saw a 0.1% quarterly rent increase to US$26.1/sqm/month, though this remained 3.3% lower YoY. Occupancy rates grew to 90.5% (up 3% QoQ and 0.3% YoY).

Grade A led in rent recovery while Grade B dominated absorption. This shows tenants still value premium spaces but are increasingly cost-conscious, driving demand for budget-friendly options.

Outlook

From 2026 to 2031, HCMC’s office market expects ~626,000 sqm of new supply. Through the rest of the year, average rents may see a slight adjustment due to this influx, alongside inflationary and exchange rate pressures.

HCMC Retail Performance

Supply

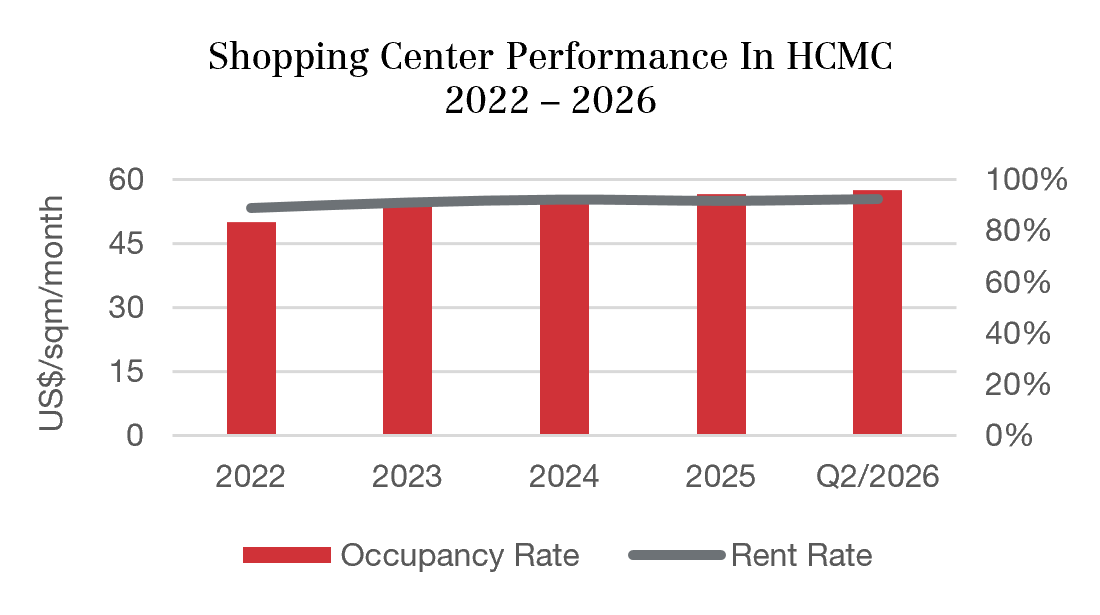

With no new retail mall developments completed in Q2/2026, HCMC’s total retail supply remained stable at around 1.1 million sqm.

Performance

The retail real estate sector remained stable throughout Q2/2026. Market occupancy climbed to 96%, reflecting a 0.6% sequential increase from Q1/2026 and a 1.8% improvement YoY. Most retail supply absorption occurred in central area, tightening available CBD supply.

Overall, average rental rate reached US$55.3/sqm/month for all-area. Meanwhile, rent rates for malls in CBD area fluctuated between US$150-$280 in Q2/2026.

In Q2/2026, selected F&B brands in HCMC continue to shift from street-front locations toward shopping malls to capitalize on stable footfall and more efficient operating conditions. Meanwhile, several restaurants have temporarily closed selected branches in shopping centers for renovation. This reflects their commitment to upgrading store quality, enhancing customer experience, and boosting long-term market competitiveness.

Outlook

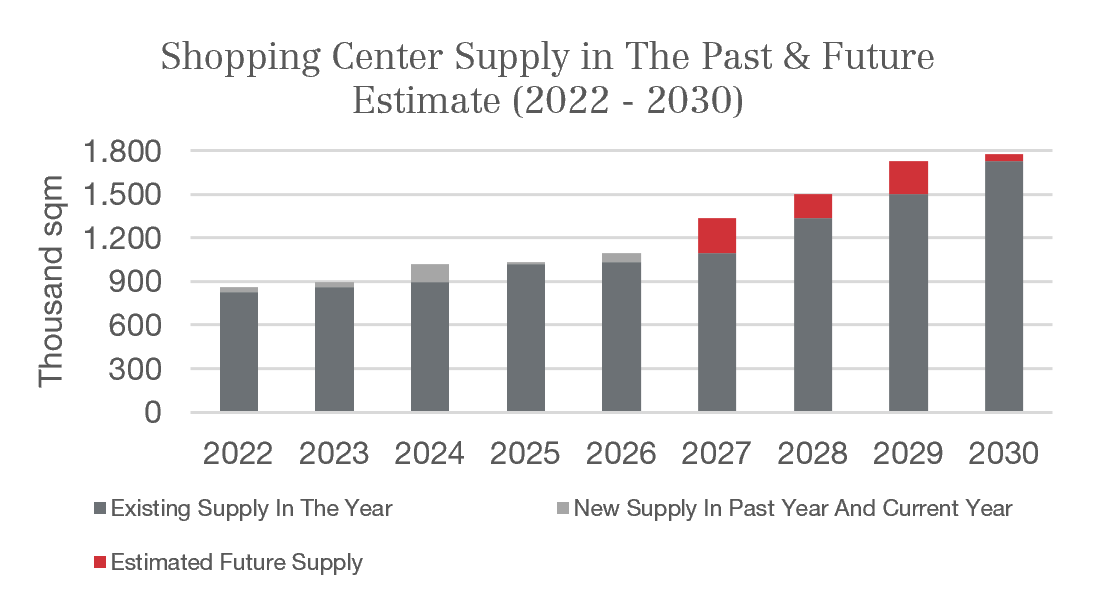

During 2026–2031, greater HCMC (including Tay Ninh and Dong Nai) expects approximately 903,000 to 1,325,000 sqm of new retail supply. This pipeline will concentrate in Non-CBD hubs, driven by experiential retail, multi-channel formats, and mixed-use retail podiums. Meanwhile, major international fashion, lifestyle, and cosmetics brands continue to favor malls and shopping streets in central areas.

Southern Industrial Performance

Supply

In Q2/2026, several new industrial parks broke ground in Southern Vietnam, adding roughly 2,244.5 ha to the supply pipeline. Notably, KN Holdings commenced phase one of the KNIC Nam Long Thanh IP in Dong Nai (1,000 ha), with its second phase expected to contribute an additional 1,600 ha.

Performance

This quarter, HCMC industrial parks maintained an 80% average occupancy. Remaining RBF and RBW spaces command rents between US$4.6 and US$5.7/sqm/month. Meanwhile, vacant industrial land rates vary widely by sector: high-tech, semiconductor, and eco-friendly zones command an average of US$250–$350/sqm/lease term, whereas general industrial areas could range approximately from US$130 to US$190/sqm/lease term. Leasing activities were driven by sectors such as component manufacturing and supporting industries.

Outlook

Driven by surging orders, Vietnam’s June Manufacturing PMI rose to 51.8, signaling a positive outlook for the rest of 2026. This momentum is further backed by several late-Q2 infrastructure groundbreakings, including the Ho Tram-Long Thanh Expressway and Nguyen Huu Canh Boulevard. These new networks will significantly boost industrial development across Ho Chi Minh City and Dong Nai.

Meanwhile, global supply chain requirements from major multinational manufacturers are encouraging industrial landlords to upgrade ESG and logistics infrastructure. To help tenants seamlessly comply with ESG standards and reduce individual investment burdens, major developers like Becamex are upgrading their industrial parks with shared ESG-ecosystem infrastructure. Simultaneously, RBW and RBF owners are adopting smart logistics to align with global standards. A prime example is SuperPort Vietnam, which boosted operational productivity by ~35% by integrating AI into its logistics. In the long run, adapting to these smart, sustainable trends is crucial for industrial landlords to remain competitive.

Source: Ministry of Industry and Trade, S&P Global, Hepza, NAI Vietnam Research, VnExpress, Cafef, Tuoitre, Laodong.vn, Mekongasean

Note: See Note (3) for average infrastructure maintenance, wastewater treatment, and industrial water fees

Investment Outlook

Overview

In Q2/2026, the commercial real estate (CRE) in Vietnam is showing resilience:

- Tenant caution shaped a selective Q2/2026 office market, dividing demand between cost-effective spaces and premium, green-certified buildings in prime locations. Businesses are taking longer to finalize leases as they balance budgets with the need for collaborative and efficient layouts. Renewals and relocations served as the market drivers for this quarter.

- The long-term future retail supply will be driven by large-scale shopping malls and retail podiums within integrated mixed-use urban developments. Forward-looking, these upcoming projects in provinces such as Tay Ninh and Dong Nai, and the expanded HCMC (former Binh Duong and Ba Ria–Vung Tau), are expected to emerge as new consumer destinations, reinforcing the shift toward experiential retail models outside central areas.

- Industrial real estate is shifting toward high-tech and AI-integrated infrastructure. To attract FDI and meet upstream logistics demands, both landlords and tenants must quickly adapt to these smart manufacturing trends.

Future Outlook

Office ~33,400 sqm of new supply lands in 2026 supplied by The Kross, the only new Grade A completion. Meanwhile, from 2026 to 2031, HCMC’s office market expects approximately 626,000 sqm of new supply. Expect rents to soften alongside inflation and FX pressure.

Retail ~903,000–1,325,000 sqm is due over 2026–2031 in greater HCMC areas (including Tay Ninh and Dong Nai)— experiential formats and mixed-use podiums lead.

Industrial PMI at 51.8 and new expressway groundbreakings (Ho Tram–Long Thanh, Nguyen Huu Canh) support Dong Nai and HCMC; ESG and smart-logistics upgrades accelerate. Minimum future supply of IP land until 2036 is expected to reach 58,000 ha.

Macro A prolonged trade deficit and firm oil prices keep exchange-rate and operating-cost pressure in view.

Province Spotlight: Tay Ninh

Strategic Position

Tay Ninh province is selected as this quarter’s province spotlight due to its post-merger scale, border connectivity and logistics potential.

- Tay Ninh Province, spanning 8,536.4 km² with around 3.2 million people, holds a unique location. Bordering HCMC, it serves as a vital bridge connecting HCMC to the Mekong Delta and onward to Cambodia. This positions Tay Ninh as a key interregional logistics hub and HCMC’s important secondary growth corridor through integrated industrial, logistics, and urban development.

- With this orientation, Tay Ninh, together with HCMC as a regional financial center and Dong Nai as an industrial base, can form a strong economic triangle. Resolving infrastructure and institutional bottlenecks will unite these three pillars, fully unlocking the Southeast Region’s economic potential.

Why Tay Ninh

- Scale 8,536 km² and ~3.2M people after the provincial merger.

- Gateway borders HCMC; bridges to the Mekong Delta and onward to Cambodia.

- Growth triangle anchors the HCMC–Dong Nai–Tay Ninh corridor.

Terminology & Notes

Terminology

AI: Artificial Intelligence

CBD: Central Business District

ESG: Environmental, Social, Governance standards

GDP: Gross Domestic Product

HCMC: Ho Chi Minh City

QoQ: Quarter-on-Quarter

LDR: Loan to Deposit Ratio

Non-CBD: Non-Central Business District

Notes

(1) Average SC of Grade A and Grade B office buildings are approximately US$7.2 and US$5.8 respectively

(2) Average SC of Retail is approximately US$5 – US$15 (approximately 10% – 25% of rental rate)

(3) RBF/RBW: Infrastructure maintenance fee: 0.8 – 4.8 USD/m²/year; Water & Wastewater (Combined) fee: 0.40 – 8.40 USD/m³

IP Land: Infrastructure maintenance fee: 0.04 – 4.8 USD/m²/year; Water & Wastewater (Combined) fee: 0.78 – 8.40 USD/m³

(Green, high-tech industrial parks typically have fees that fall within the higher end of the price range.)

(4) Adjusted Grade A & B Rents (US$, excluding SC) to better reflect market-wide averages:

This research has been prepared by NAI Vietnam for informational purposes only and should not be considered investment or legal advice.

This research report has been prepared independently and solely on the basis of publicly available information that NAI Vietnam considers to be reliable but NAI Vietnam has not independently verified the contents hereof. NAI Vietnam accepts no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts and reflect their opinion as of the date hereof. These opinions are subject to change and NAI Vietnam does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without NAI Vietnam’s prior written consent.

+84 901 665 445 | info@naivietnam.com | naivietnam.com