Economic Outlook

In Q3/2025, the national Gross Domestic Product (GDP) has an estimated growth of 8.2% YoY. The industrial and construction sector continued to be the main driving force, increased by 9.5% YoY.

Vietnam attracted a total FDI of approximately US$ 28.5 billion after 9 months, marking a significant 15.2% increase compared to the same period and representing a sustained high, building on the momentum from the beginning of the year.

The number of newly established companies and those resuming operations reached 27,500 (up 55.6%) in September. For the nine-month period, the figure reached over 231,300 enterprises (an increase of 26.4%).

The number of enterprises withdrawn from the market over the nine-month period increased by 6.8%. These indicators suggest significant improvement in the overall business and economic environment.

Following the recent provincial merger, Vietnam’s growth outlook in the CRE sector appears stronger. More specifically, the expansion of Ho Chi Minh City (HCMC) create favorable development conditions by driving significant transaction volume, while simultaneously raising regional retail standards and streamlined logistics governance. In turn, infrastructure planning should accelerate to support the city’s expanded economic base.

Office Performance

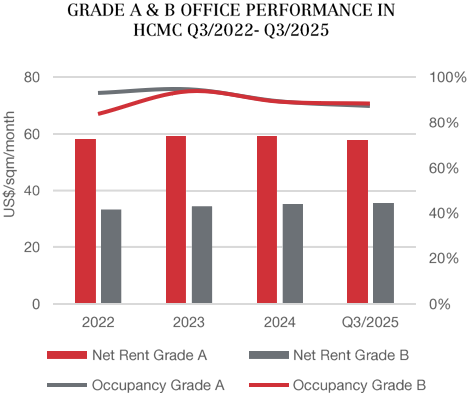

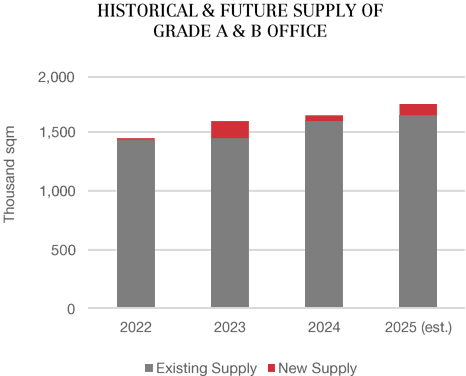

Stable Supply

In Q3/2025, the supply of Grade A and Grade B offices in pre-merger HCMC increased with the opening of Saigon Marina IFC, bringing the total supply to over 1.7 million square meters.

Weaker Performance

The average net rental rate for Grade A softened by 1.3% QoQ and 1.4% YoY, settling at US$ 58.4/sqm/month. The occupancy of Grade A reached 87.3%, down 2.6 ppts QoQ and 2.3 ppts YoY.

The reduction of Grade A performance was largely due to the introduction of new supply, which usually requires at least two years to fill up vacancy.

Meanwhile, Grade B rents held around US$ 35.6/sqm/month, eased 0.9% QoQ but increased 1.1% YoY. Occupancy stood at 88.3%, a slight decrease at 0.6 ppt QoQ and 1 ppt YoY.

Grade B performance recorded a slight decline, with pressure from aging assets requiring renovation and expiring land-use rights at certain properties.

Outlook

After provincial merger among HCMC, Ba Ria-Vung Tau and Binh Duong, the market has recorded several large office lease transactions as leading companies scale up or relocate from neighboring provinces into HCMC’ Central Business District (CBD). This trend is expected to persist in the near term.

Retail Performance

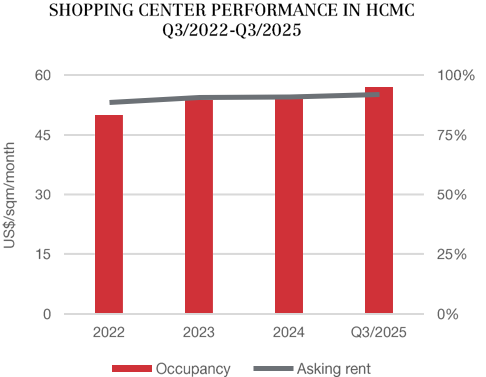

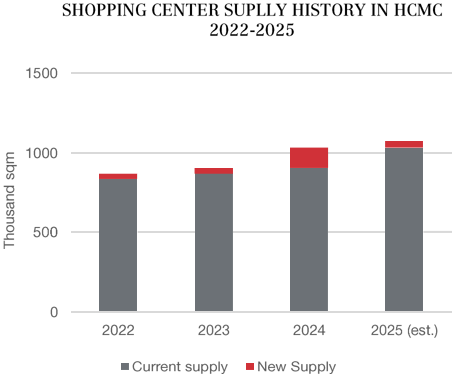

Stable Supply

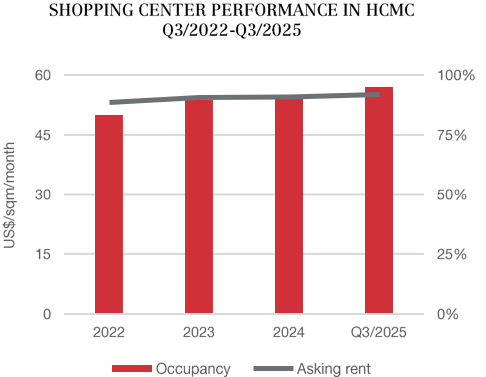

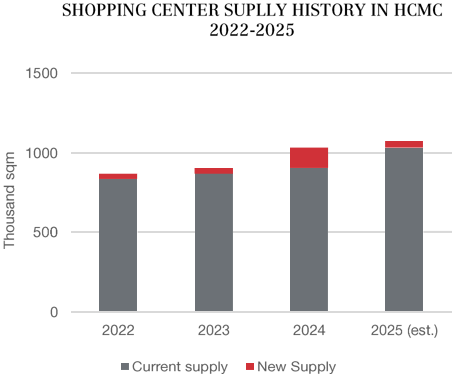

In Q3/2025, shopping centers in pre-merger HCMC saw no additional supply, leaving total stock unchanged at nearly 1.1 million sqm.

Positive Performance

This quarter recorded an increase in the performance of shopping centers in pre-merger HCMC. The average asking rent price is US$ 55.2/sqm/month in Q3/2025, experienced a raise of 0.6% QoQ and 1.2% YoY. The market-wide occupancy rate reached 95%, increased by 1.2 ppt QoQ and 5.2 ppt YoY. Occupancy in the CBD remained at 100%, supported by the absence of new supply this quarter.

Outlook

Q3/2025 saw a clear resurgence of activity in HCMC, led by F&B and cosmetics brands actively opening stores and expanding leased space in prime locations, signaling stronger confidence in household spending and the market’s long-term potential. Specifically, post-merger, the retail standards in Binh Duong and Ba Ria – Vung Tau are expected to raise. This occurs as local malls in these areas must compete with HCMC’s premium standards in operations and design, benefiting consumers with better brands, diversified offerings and improved service.

Industrial Performance

Stable Supply

Vietnam’s industrial real estate supply expanded significantly in Q3/2025 following large-scale project approvals after provincial mergers. Key southern additions include Thu Thua Industrial Park (171 ha), Binh Hoa Nam 1 Industrial Park (322 ha), and Xuyen A Industrial Park Phase 3 (177 ha) in Tay Ninh. In the North, Phu Tho, Thai Nguyen, and Hai Phong are leading the expansion with new projects ranging from 186 to nearly 300 ha, collectively adding thousands of hectares to the national industrial land supply.

Positive Performance

Import and export in 9 months reached over 680 billion USD, up 17.3% over the same period; trade surplus 16.8 billion USD. This strong inflow, primarily concentrated in the maunfacturing and processing industries, has provided a significant growth catalyst for the industrial real estate segment, boosting demand for industrial land and ready-built factories. Besides, tenant preferences are shifting toward high-grade ready-built factories designed for flexibility and compliance with light- and mid-industry requirements.

Outlook

Vietnamese industrial base is set to move further up the global value chain, backed by automation and streamlined industrial-logistics governance. Unified logistics corridors and streamlined provincial governance are shortening distance and simplifying procedures, making previously “frontier” locations more attractive to investors. Thus, widening the map for industrial manufacturers and logistics operators. Regarding automation, initiatives such as the Vietnam Automation Center of Excellence in Ho Chi Minh City (HCMC) serve as critical bridges between manufacturers, technology providers, and subject-matter experts.

Investment Outlook

Overview

Vietnam’s commercial real estate (CRE) market in Q3/2025 continues to draw attention, supported by steady FDI flows, solid economic growth, and ongoing infrastructure investment. For investors, opportunities lie in upgrading and repositioning older properties, with ESG compliance increasingly shaping long-term value.

- Prime offices are outperforming, while aging stock struggles under competitive pressure. High renovation costs are pushing some owners to sell, creating redevelopment opportunities for investors.

-

The industrial real estate remains stable, with land prices on a steady upward trajectory. Investors are encouraged to move early into emerging locations, capturing value before the next pricing wave.

- Retail real estate is showing gradual improvement, led by strong demand from F&B tenants. For investors and developers, this creates an opportunity to capture growth — but success will hinge on well-researched rental strategies that align with evolving visitor needs and spending habits.

Highlighted Province

Gia Lai (merged with Binh Dinh since July 2025) is the choice of Q3-2025:

-

With an area of 21,000 km², a population of 3.6 million people – it is one of provinces with the largest area and population in the country.

-

Oriented to become a center for food processing, manufacturing, renewable energy, and high-tech agriculture.

-

Has strategic connectivity, linking the North to the South of Vietnam, from Quy Nhon Port in the east to Laos and Cambodia in the west.

Inquiries Handled by NAI Vietnam

NAI Vietnam has received more inquiries, especially from the Northern region:

This research has been prepared by NAI Vietnam for informational purposes only and should not be considered investment or legal advice.

This research report has been prepared independently and solely on the basis of publicly available information that NAI Vietnam considers to be reliable but NAI Vietnam has not independently verified the contents hereof. NAI Vietnam accepts no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts and reflect their opinion as of the date hereof. These opinions are subject to change and NAI Vietnam does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without NAI Vietnam’s prior written consent.

+84 901 665 445 | info@naivietnam.com | naivietnam.com