Vietnam’s commercial real estate market opened 2026 on solid footing, supported by strong macroeconomic growth and continued foreign investment inflows. Below is a snapshot across the office, retail, and industrial segments, along with the broader economic and investment outlook.

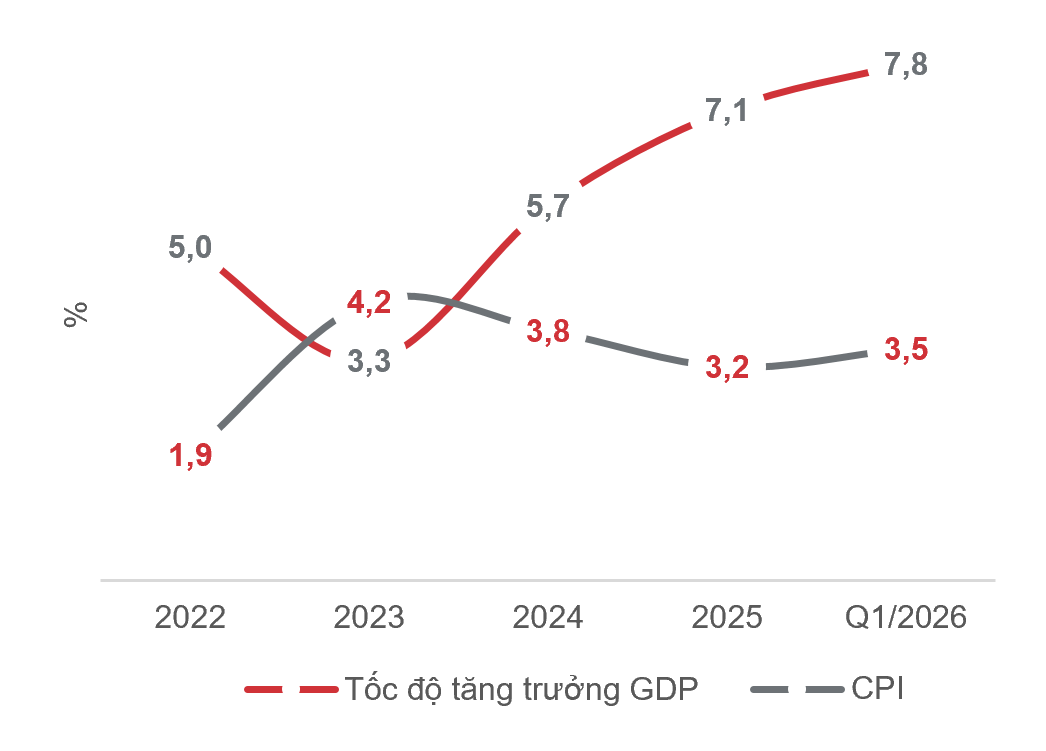

Vietnam’s GDP growth in Q1/2026 reached 7.8%, with gains recorded across all three sectors: agriculture, forestry, and fisheries rose 3.6%, industry and construction climbed 8.9%, and services expanded 8.2%. Retail sales of consumer goods and services reached US$72.2 billion, up 10.9% year-on-year, driven by strong domestic consumption around Lunar New Year and a high volume of international visitors.

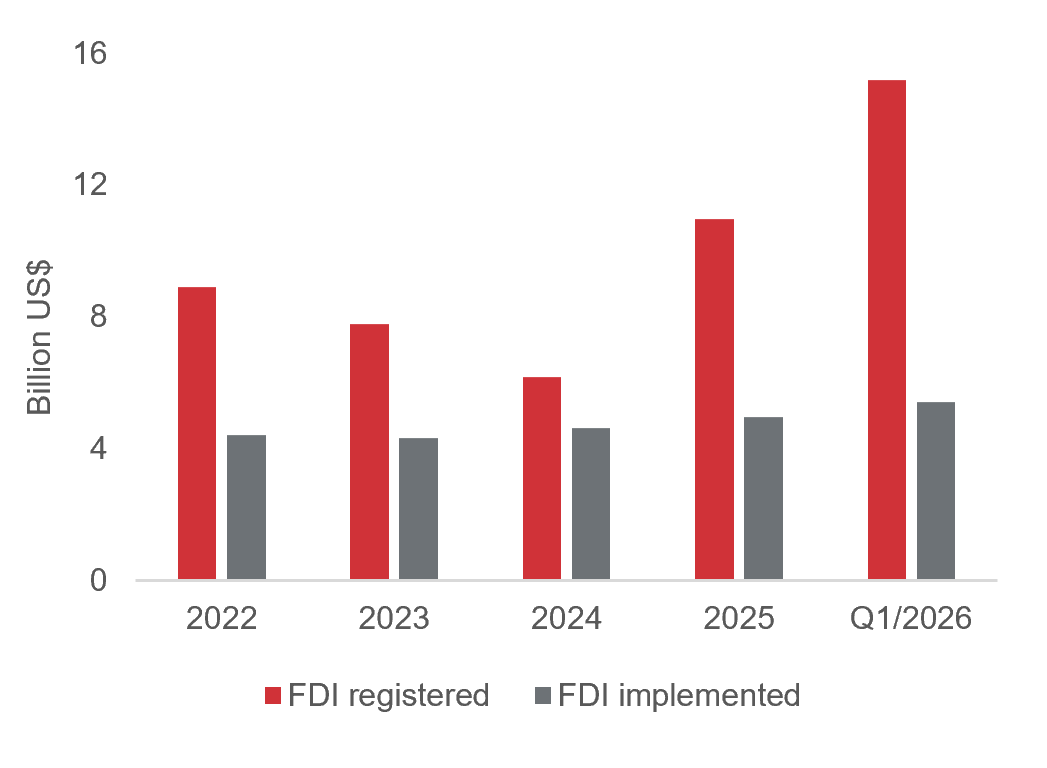

Foreign direct investment also accelerated, with Vietnam attracting US$15.2 billion, a 42.9% increase year-on-year. Processing and manufacturing remained the dominant sector, absorbing 82.8% of newly implemented capital, while real estate ranked second at US$389.5 million (7.2% of the total).

The quarter also saw 96,000 new or resumed businesses, against roughly 91,800 market exits, pointing to intensifying competitive pressure. Heightened global geopolitical tensions, particularly in the Middle East and Gulf region, continue to pose external risks to trade flows, input costs, and overall economic stability in the quarters ahead.

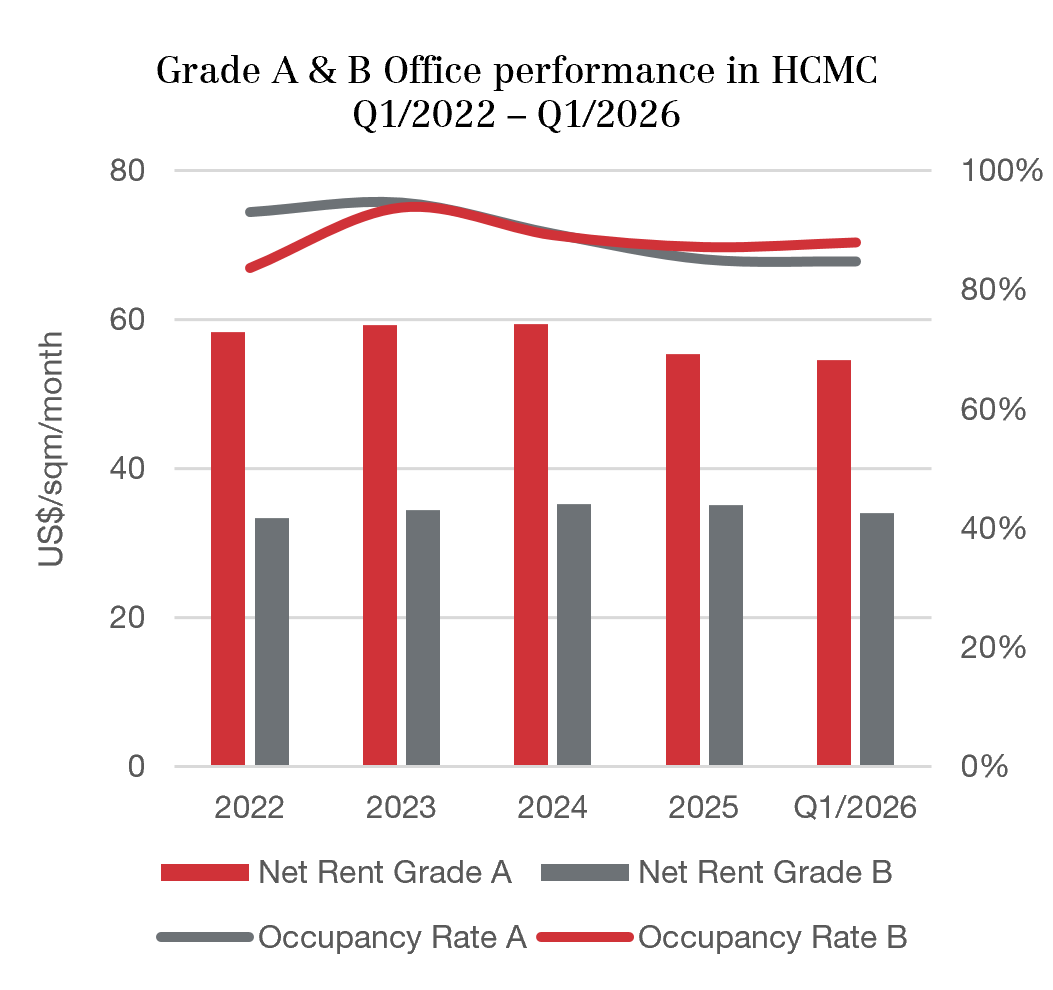

No new office supply entered Ho Chi Minh City in Q1/2026, keeping total stock stable at over 1.8 million sqm. Grade A average rents eased 0.9% quarter-on-quarter and 1.4% year-on-year to US$54.5/sqm/month, while occupancy edged up 0.9% quarter-on-quarter to 84.6% — though still down 0.4% year-on-year, signaling that prior-year supply has not yet been fully absorbed.

Grade B rents fell 0.7% quarter-on-quarter and 3% year-on-year to US$33.9/sqm/month, while occupancy rose to 87.9%, reflecting growing tenant demand for more cost-efficient options as businesses prioritize operational efficiency.

Looking ahead, global uncertainty may weigh on short-term leasing demand even as new supply continues to enter the market, making operational efficiency, flexible pricing, and proactive tenant retention key priorities for landlords.

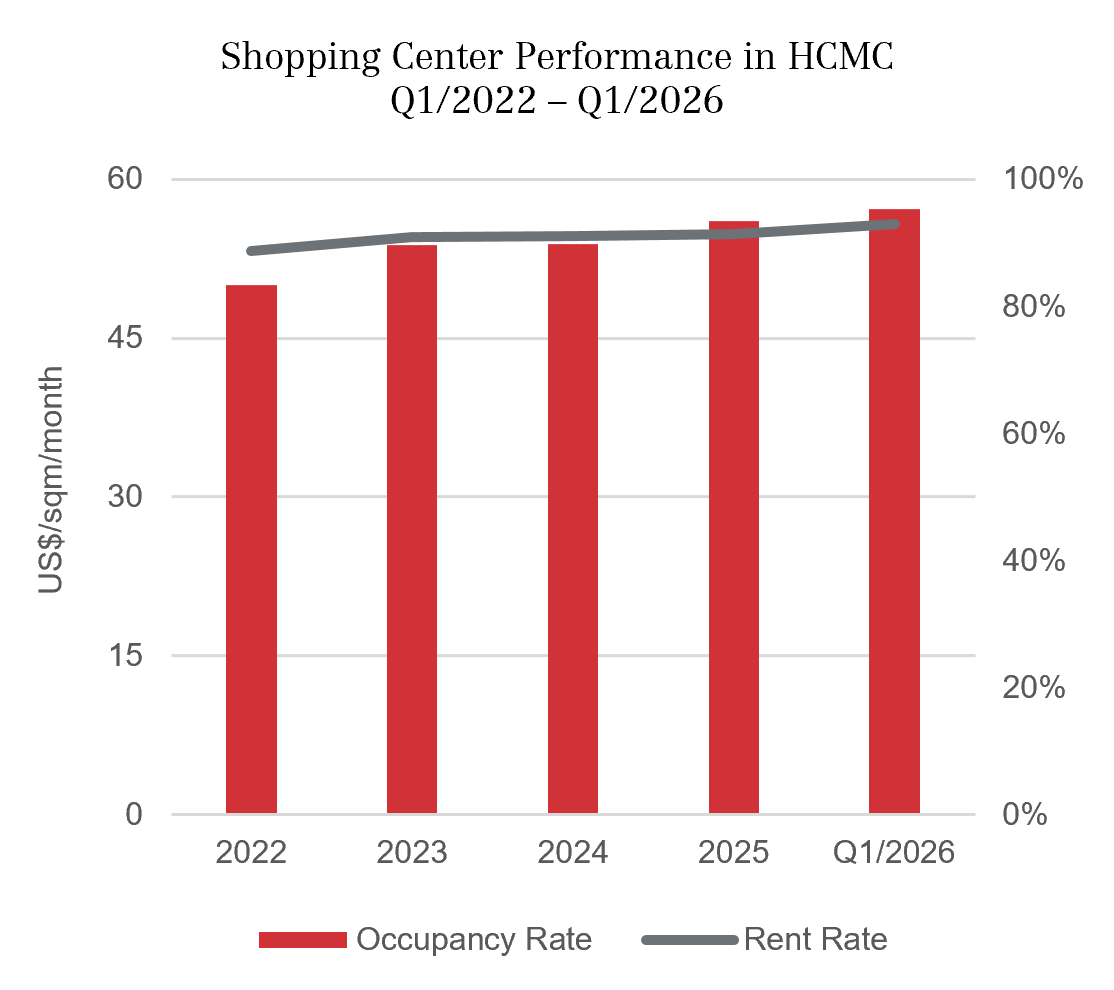

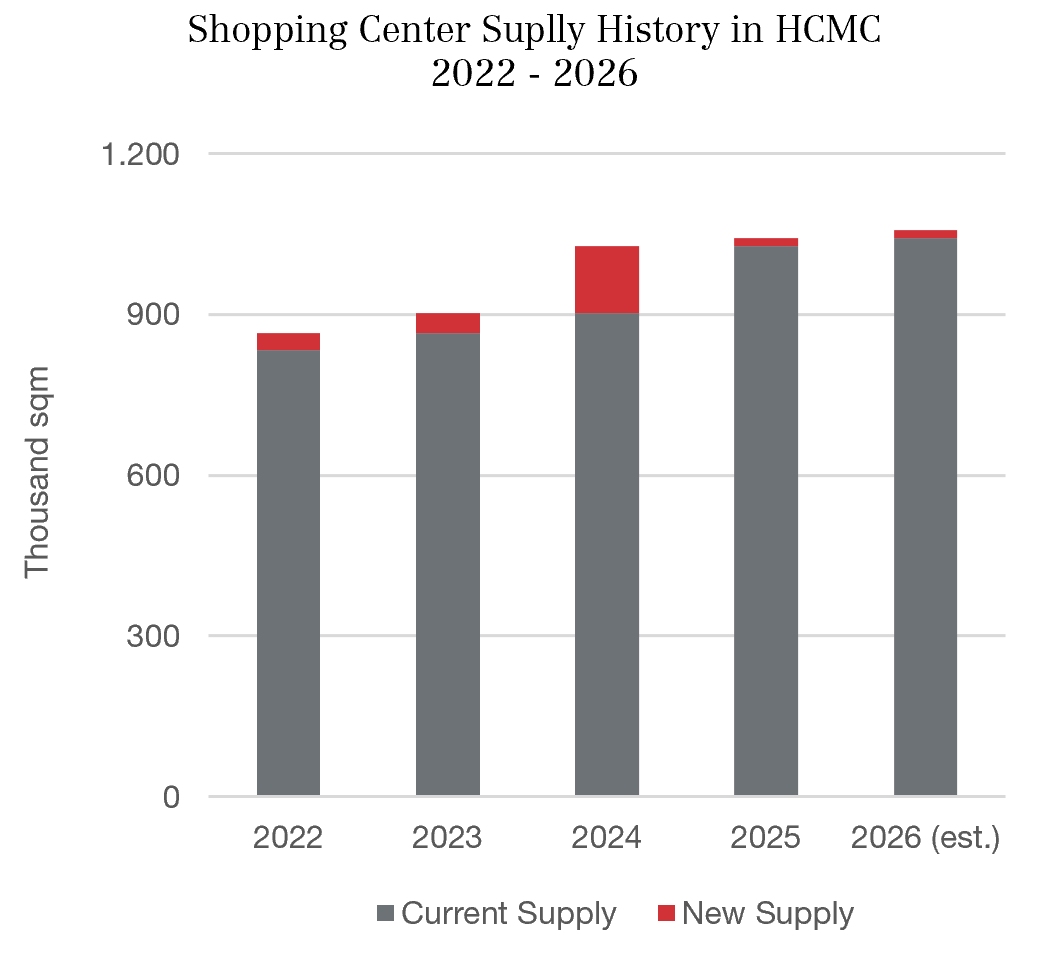

Retail mall supply in Ho Chi Minh City held steady at approximately 1.1 million sqm, with no new completions in the quarter. Occupancy continued its upward trend, reaching 95.4% — up 0.4% quarter-on-quarter and 2% year-on-year, led by stronger performance at non-central malls. Average asking rents rose to US$55.8/sqm/month, up 1.4% quarter-on-quarter and 1.8% year-on-year.

The retail landscape is shifting as international brands increasingly favor lifestyle and interactive store formats over traditional retail chains, leveraging fast turnover and youth-oriented designs to sustain footfall despite rising rental costs.

Industrial land supply expanded in the quarter, led by new project groundbreakings in northern Vietnam, including My Thai Industrial Park (160 ha, Bac Ninh), Minh Duc – Thuong Lan – Ngoc Thien Industrial Park (163 ha, Hung Yen), and Hai Long VSIP Ninh Binh (180 ha). Southern Vietnam saw more measured activity, focused on planning and regulatory groundwork.

The Industrial Production Index rose 9% year-on-year in the first three months, fueled by a 9.7% increase in manufacturing and processing, with particularly strong growth in Ninh Binh, Phu Tho, Bac Ninh, Thai Nguyen, and Hai Phong.

Sustainability is becoming a defining theme: Phu My 3 Specialized Industrial Park, selected as a pilot eco-industrial model, completed Phase 1 and is finalizing certification to become Ho Chi Minh City’s first certified eco industrial park in Q1/2026 — part of a broader shift toward green and smart industrial parks to meet international standards and attract higher-quality FDI.

Green transformation is accelerating across Vietnam’s commercial real estate sectors. Office buildings face growing pressure to upgrade toward green standards and technology integration to remain competitive, while many shopping centers are adopting sustainable construction materials and solar power systems to boost efficiency and brand value. In industrial real estate, ESG compliance is increasingly a prerequisite for participating in global supply chains.

Dong Nai province — newly merged with Binh Phuoc as of July 2025 — is this quarter’s highlighted growth region. As a key economic hub in Southeast Vietnam with a population of 4.4 million across more than 12,700 km², the province is home to Long Thanh International Airport, positioning it as a convergence point for industrial, logistics, urban, trade, and aviation development. Its transition into a centrally governed city is expected to further unlock its economic and infrastructure potential.